Payment gateways power payments across online, mobile and in-store channels. This guide explains how they work, why omnichannel matters in 2026, and what merchants must prepare for.

Payment gateways have evolved from simple online transaction processors into sophisticated omnichannel platforms that power commerce across every customer touchpoint. What is a payment gateway? At its core, it’s the technology infrastructure that securely authorizes and processes payments between customers and merchants, whether transactions happen online, in-store, or through mobile devices.

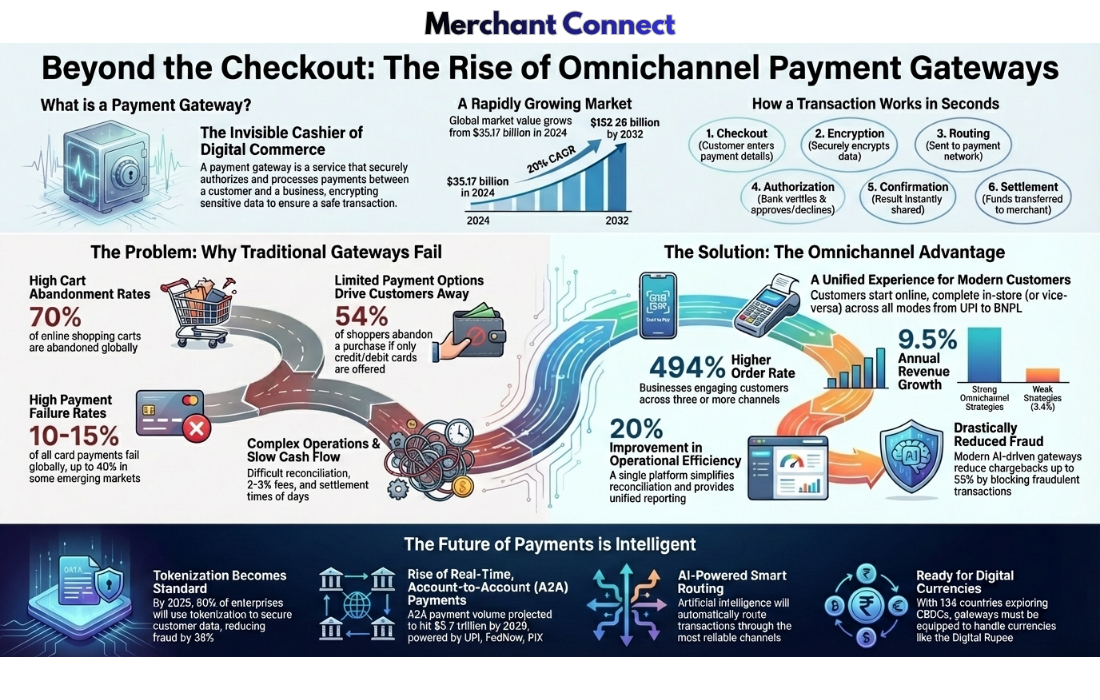

The stakes have never been higher. The global payment gateway market reached $35.17 billion in 2024 and is projected to surge to $152.26 billion by 2032, representing a compound annual growth rate of 20%. This explosive growth reflects a fundamental shift in how consumers shop and how merchants must operate to remain competitive.

Why Omnichannel Payment Capabilities Matter

Modern consumers don’t think in channels—they think in experiences. Consider these merchant-critical statistics:

- Retail customers now use an average of six different touchpoints before completing a purchase, up from just two touchpoints 15 years ago.

- Merchants with strong omnichannel engagement strategies retain 89% of customers, compared to those using single-channel approaches.

- Multichannel shoppers spend four times more than in-store-only customers and ten times more than online-only customers.

- 67% of consumers expect buy-online-pickup-in-store (BOPIS) capabilities as a standard offering.

For merchants, the message is unambiguous: fragmented payment systems lead to lost revenue, operational inefficiency, and customer churn. Unified omnichannel payment gateways are no longer a competitive advantage—they’re a business necessity.

What is a Payment Gateway? Understanding the Merchant Infrastructure

A payment gateway is a merchant service that authorizes and processes payments for online and offline transactions. It acts as the intermediary between your business, customers, acquiring banks, card networks, and issuing banks, ensuring every transaction is encrypted, authenticated, and settled securely.

Explainer video: What is a Payment Gateway? — Merchant Connect

How Payment Gateways Work: A Merchant’s Perspective

Understanding the payment flow helps merchants optimize acceptance rates and reduce processing costs. Here’s what happens in seconds during each transaction:

- Step 1: Customer Initiates Payment — A customer selects their payment method—credit card, debit card, UPI, digital wallet, or bank transfer—and submits their payment credentials through your checkout interface.

- Step 2: Data Encryption and Transmission — The payment gateway immediately encrypts the sensitive payment data using SSL/TLS protocols and transmits it securely to your acquiring bank.

- Step 3: Authorization Request Routing — Your acquiring bank forwards the authorization request through the appropriate card network (Visa, Mastercard, RuPay, American Express) or payment rail (UPI, RTGS, NEFT) to the customer’s issuing bank.

- Step 4: Fraud Detection and Risk Assessment — Advanced gateways employ AI-powered fraud detection systems that analyze hundreds of data points in milliseconds.

- Step 5: Issuer Authorization — The issuing bank verifies funds/credit and approves or declines the transaction.

- Step 6: Response and Confirmation — The authorization response travels back through the chain and the customer receives immediate confirmation.

- Step 7: Settlement and Reconciliation — Approved transactions are batched and settled; funds transfer to the merchant account within 24–72 hours depending on agreements.

The Critical Limitations of Traditional Payment Gateways

Legacy payment gateways, designed primarily for e-commerce card transactions, create significant challenges for modern merchants operating across multiple channels.

Revenue Impact of Gateway Limitations

Cart Abandonment Crisis — Globally, 70% of online shopping carts are abandoned before purchase completion. Payment friction ranks as one of the top three abandonment causes, with merchants losing an estimated $18 billion annually to preventable checkout issues.

Payment Method Restrictions — Research shows 54% of customers will abandon their purchase if their preferred payment method isn’t available. Traditional gateways often support limited payment options, forcing merchants to integrate multiple providers and creating fragmented customer experiences.

Failed Transaction Rates — Card payment failure rates range from 10–15% in developed markets and can exceed 40% in emerging economies. Each failed transaction represents direct revenue loss and damaged customer relationships. Merchants using basic gateways lack the intelligent routing capabilities needed to optimize authorization rates.

Trust and Security Concerns — Approximately 25% of customers abandon checkout when payment interfaces appear untrustworthy or unfamiliar. Merchants need payment gateways that maintain consistent branding and demonstrate security credentials throughout the payment process.

Operational Inefficiencies That Hurt Merchant Profitability

Complex Reconciliation — Managing separate systems for online payments, in-store POS transactions, mobile app purchases, and recurring subscriptions creates reconciliation nightmares. Finance teams spend hours manually matching transactions across platforms, increasing operational costs and error rates.

High Processing Fees — Without intelligent routing and optimization features, merchants pay premium rates even when cheaper processing options exist.

Delayed Settlements — Cash flow suffers when settlements take three to five business days. For growing merchants, delayed access to working capital can constrain inventory purchasing and business expansion.

Siloed Reporting — When payment data lives in separate systems for each sales channel, merchants lose visibility into total business performance and struggle to identify trends, optimize operations, or make data-driven decisions.

Omnichannel Payment Gateways: The Unified Solution Merchants Need

An omnichannel payment gateway integrates all payment acceptance channels—e-commerce, mobile apps, physical stores, marketplace platforms, and subscription billing—into a single unified platform. This consolidation delivers measurable improvements to both customer experience and merchant operations.

How Omnichannel Gateways Transform Merchant Capabilities

- Unified Payment Acceptance — Process cards, UPI, wallets, net banking, BNPL and more through one system.

- Cross-Channel Transaction Visibility — View transactions, refunds, chargebacks and settlements across every channel in a single dashboard.

- Consistent Customer Experience — Start on one channel, finish on another (BOPIS, cross-device sessions) with shared tokenization.

- Intelligent Payment Routing — Smart routing algorithms choose the optimal processor/network path to improve authorization and lower cost.

- Tokenization — Save credentials once and reuse across channels while reducing PCI scope.

Measurable Business Impact for Merchants

- Revenue Growth — Merchants using three or more connected sales channels see 494% higher order rates vs single-channel operations.

- Conversion Rate Improvement — BNPL increases conversions 25–30%; smart routing and payment optimization reduce declines.

- Operational Efficiency Gains — Unified reconciliation improves finance productivity ~20%+.

- Fraud Reduction — AI-driven fraud reduces chargebacks up to 55%.

- Customer Lifetime Value — Omnichannel customers show ~30% higher LTV.

Industry-Specific Applications: Where Payment Gateways Create Merchant Value

Retail and E-Commerce Merchants

Unified inventory and payment systems for BOPIS, consistent pricing and promotions, mobile POS for line-busting, and integrated loyalty across channels.

Marketplace and Platform Merchants

Split settlements, escrow, automated commissions, and instant division of proceeds between platform and sellers.

Subscription and Recurring Billing

Tokenization, smart retry logic, autopay and dunning reduce involuntary churn by 20–30%.

Education, Financial Services & Government

Flexible fee collection, split settlements, bulk payouts, multi-language support and audit trails for transparency.

The Future of Payment Gateways: Emerging Trends Merchants Must Prepare For

Real-Time Payment Networks, AI and ML, tokenization, CBDCs, embedded finance and invisible payments are among the forces merchants must prepare for. These trends change costs, settlement timing, fraud dynamics, and integration requirements.

Choosing the Right Payment Gateway: Evaluation Criteria for Merchants

Technical Capabilities

Integration flexibility, APIs, SDKs, pre-built plugins, and mobile SDKs matter. Confirm omnichannel is unified, not separate products with separate tokenization and reports.

Business Considerations

Pricing (transaction fees, monthly fees, setup fees), settlement terms (T+0, T+1, T+2), and merchant support availability should guide your choice.

Compliance & Security

PCI DSS Level 1, ISO 27001, SOC 2, and regulatory compliance (RBI, PSD2) are essential. Evaluate built-in fraud tools and customization of fraud rules.

Reporting & Data

Real-time dashboards, export capabilities, automated reconciliation and API access to raw data enable better finance and operations performance.

Implementation Best Practices: Maximizing Payment Gateway Performance

Optimization Strategies

- Prioritize payment methods that maximize conversion and success probability.

- Optimize checkout flow: minimize fields, allow guest checkout, show accepted payment badges.

- Mobile optimization: responsive checkout, mobile wallets, biometric authentication.

- Testing & monitoring: monitor authorization rates, track decline reasons and test checkout configurations.

Security Best Practices

- Tokenization to reduce PCI scope.

- 3D Secure 2.0 for frictionless authentication.

- Regular fraud rule calibration to balance false declines vs fraud loss.

Conclusion: The Strategic Imperative of Omnichannel Payment Infrastructure

Payment gateways have transformed into strategic business platforms that directly impact revenue, customer satisfaction, operational efficiency, and competitive positioning. For merchants operating in 2025’s complex retail environment, the question isn’t whether to adopt omnichannel payment capabilities—it’s how quickly you can implement them.

The payment gateway you choose becomes part of your competitive moat. Select wisely, implement thoroughly, and optimize continuously to maximize the return on this critical infrastructure investment.

Frequently Asked Questions About Payment Gateways for Merchants

What is a payment gateway and why do merchants need one?

A payment gateway is the technology infrastructure that authorizes and securely processes payments between customers and merchants. Merchants need gateways to accept electronic payments, ensure security, comply with regulations, and receive settlements.

What’s the difference between a payment gateway and a payment processor?

The gateway collects and transmits payment information securely. The processor handles authorization and settlement with card networks and banks. Modern providers often bundle both.

How long does integration take?

Plugins (Shopify/WooCommerce) can go live in days; custom API integrations usually take 2–6 weeks; complex omnichannel implementations may take 2–3 months.